Bank Churn Prediction 💰

Project Date: February 2025

Category: Business Intelligence

Project Overview

Objective: Identify top predictors of customer churn and build an interpretable model to support retention strategy.

Data: Proprietary customer dataset (age, credit score, balance, tenure, etc.)

Methods:

- Churn-weighted feature scoring

- Volatility ranking via standard deviation

- Manual decision tree modeling (Lucidchart)

- Model validation via logical split testing

TL;DR

- Not all high-churn segments are impactful—some groups churn at high rates but represent tiny slivers of the customer base.

- Sensitive or noisy fields (like credit scores and salary) should not always be imputed—sometimes leaving nulls preserves model integrity.

- Churn is concentrated among customers with ≤3 years tenure, 3+ products, and no credit card—these represent the highest-risk profile.

Recommendation: Prioritize outreach to new customers without credit cards, and reinforce loyalty among stable, long-tenure clients.

Key Insights

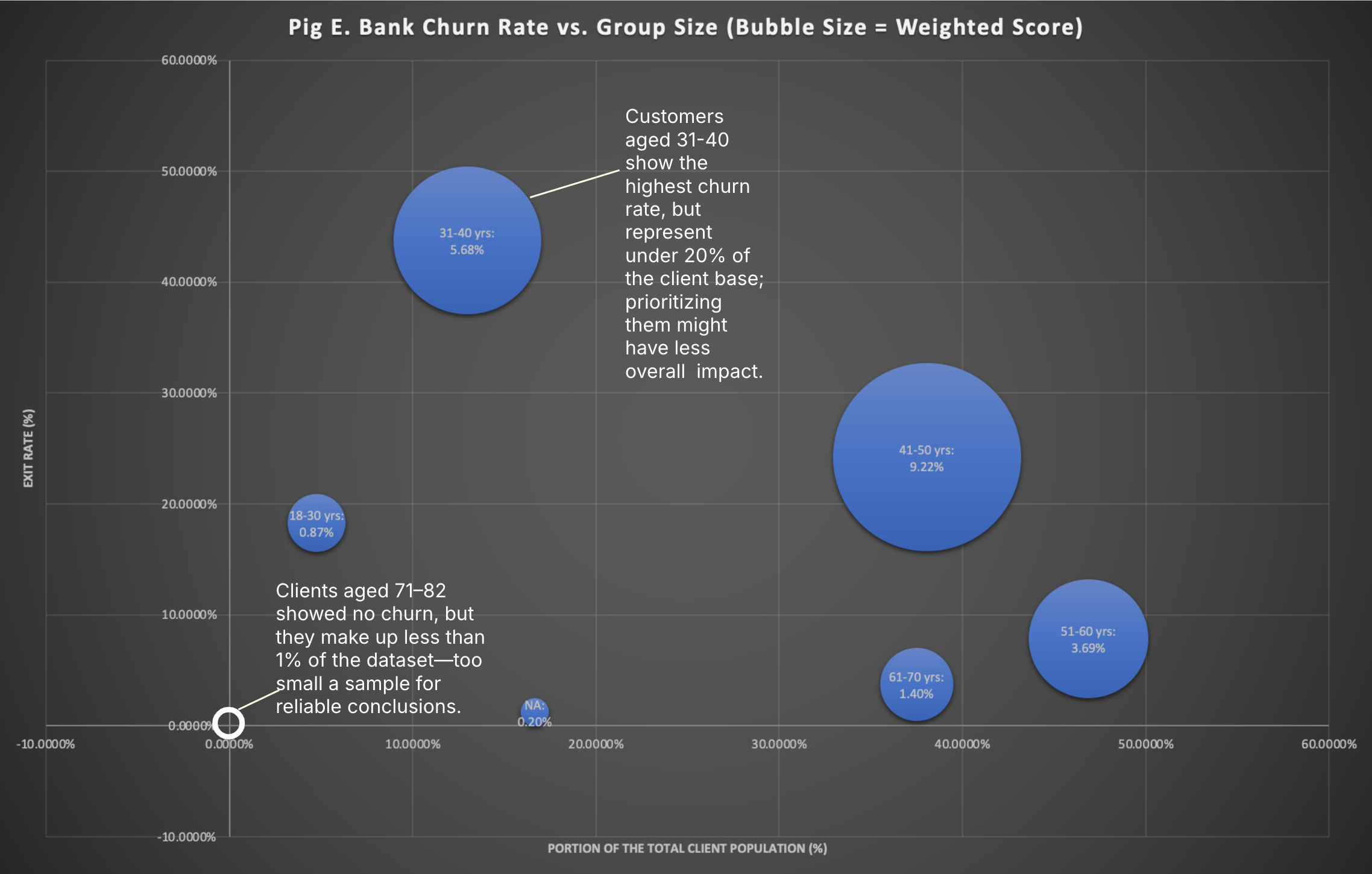

1. High Churn ≠ High Impact

Insight: Groups with high churn rates may be too small to justify targeted retention campaigns.

Example: Customers aged 31–40 have the highest churn rate, but make up less than 20% of the client base.

FIG. A: Each group’s “weighted score” multiplies churn rate by population share, to emphasize scalable risk.

⚠️ Statistical Caveat: Zero-churn groups (e.g. clients aged 71–82) are too small (<1%) for reliable modeling.

2. Don’t Always Impute—Especially for Noisy or Sensitive Variables

Credit Score: Skipped imputation—statistically opaque, ethically fraught.

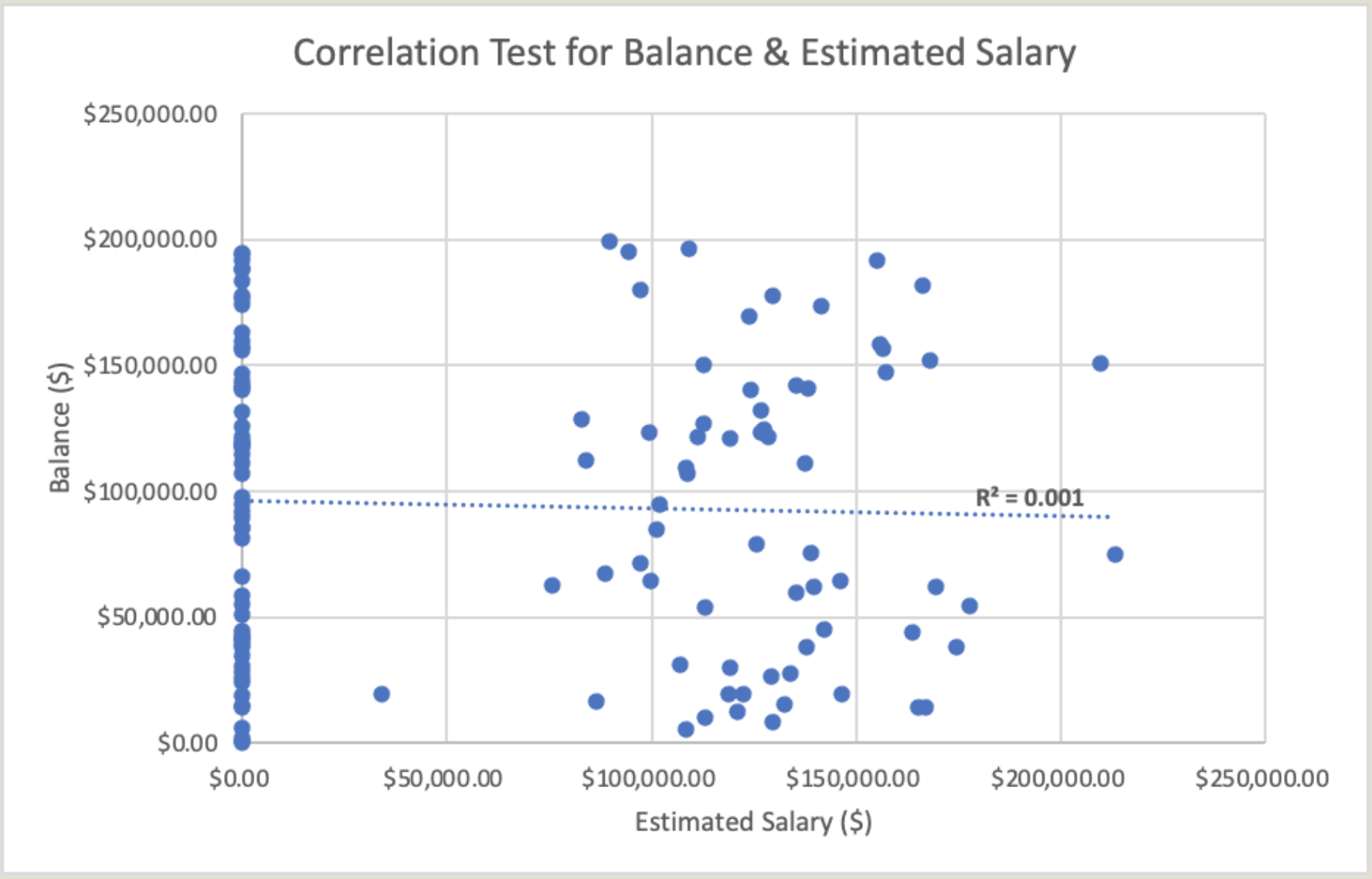

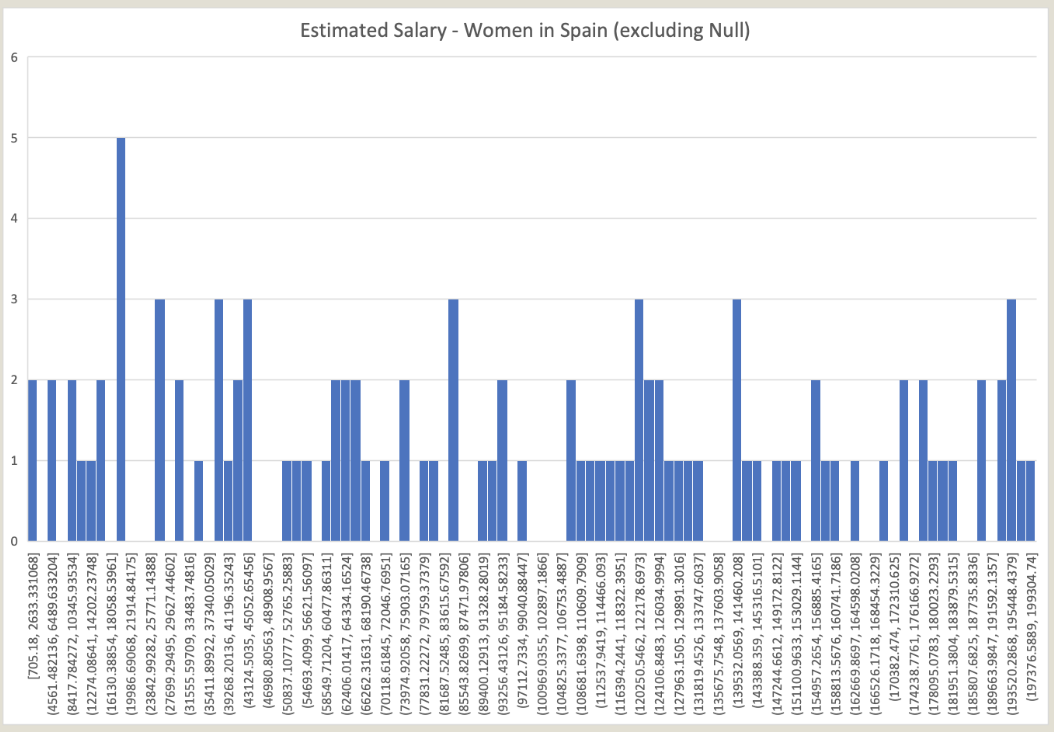

Estimated Salary:

- Tried subgroup-based fill (e.g. by gender or country)

- Small sample sizes + high variance made imputation noisy

- Linear regression ruled out (R² = 0.001 with Balance)

FIG. B: No meaningful relationship between Estimated Salary and Balance (R² = 0.001)

FIG. C: Histogram of salaries for Spanish women—no clear pattern emerged to support fill-in.

➡️ Decision: Leave NA values as-is to avoid introducing noise or false certainty.

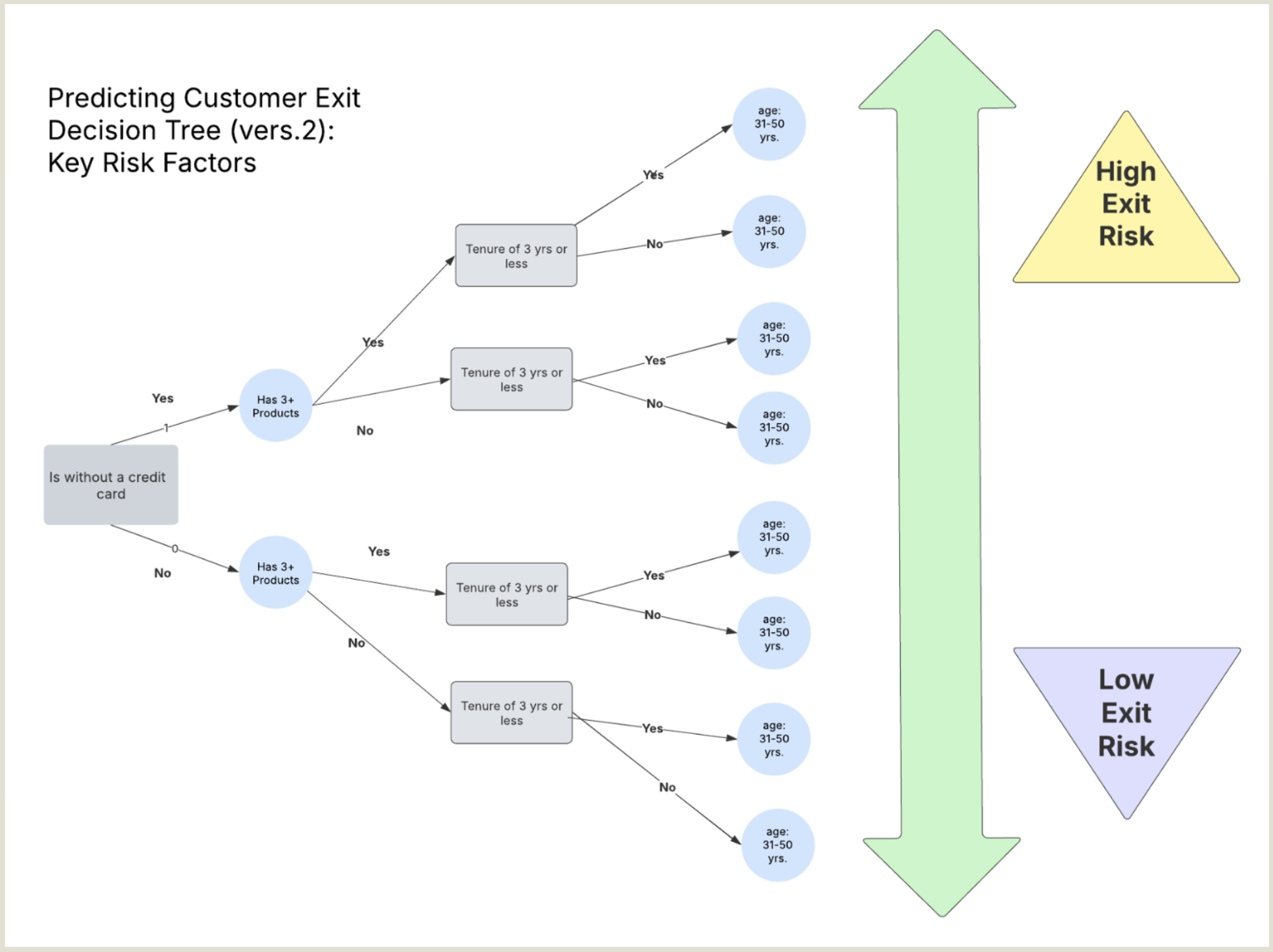

3. Top Churn Risk = No Credit Card + 3+ Products + ≤3 Years Tenure

Tree Logic:

- Split features by churn standard deviation (proxy for information gain)

- Balanced sample sizes across branches for interpretability and validation

Highest-Risk Group:

- No credit card

- 3+ products

- ≤3 years tenure

Other patterns:

- Ages 41–50 had highest weighted churn score

- 31–40 group: close second in churn and largest overall segment

- Low-tenure customers outside that age range still showed 66% churn

FIG. D: Final model structure based on validated decision splits.

Bonus: Modeling Experiment

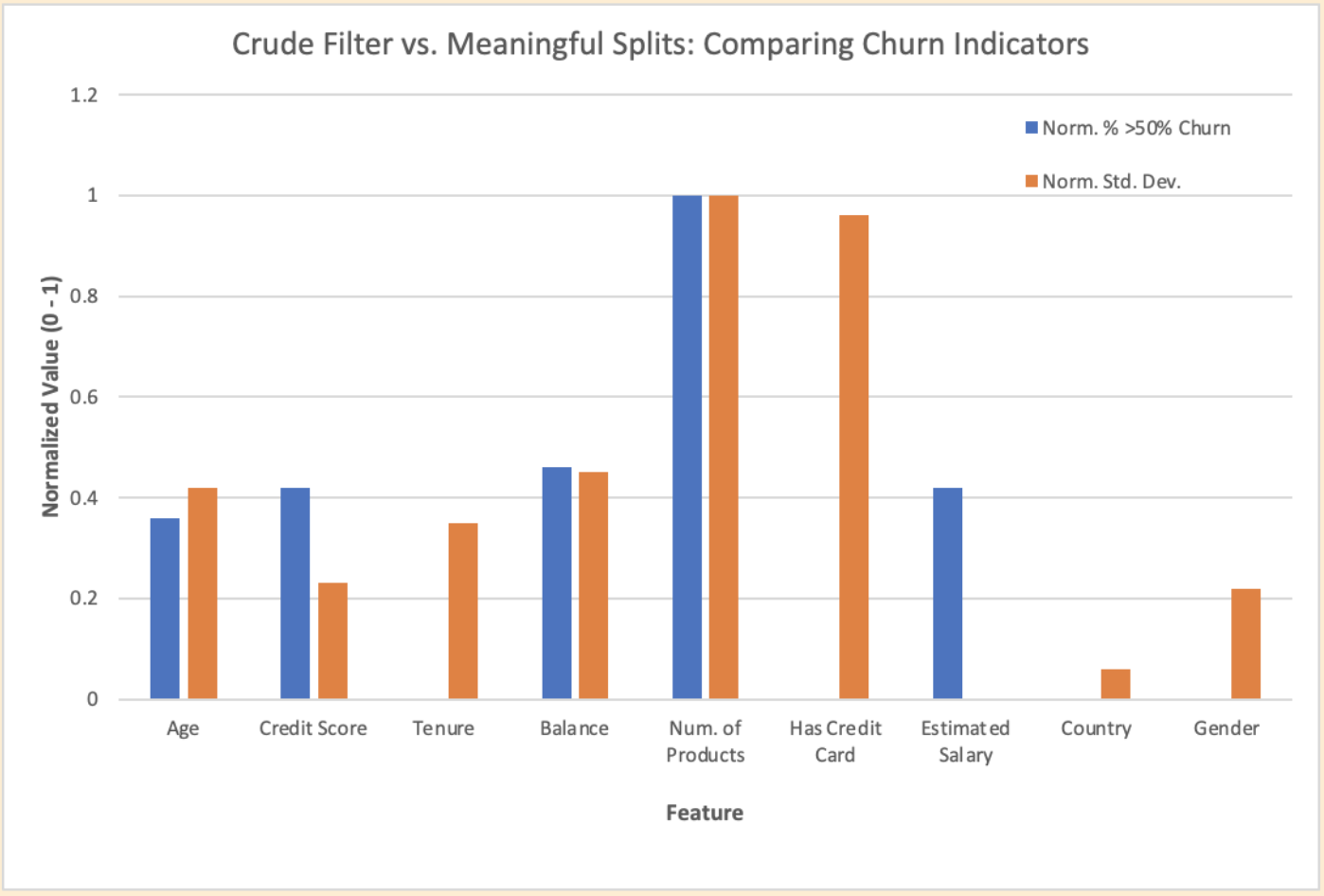

Crude Heuristic Test: “Decision Gain”

Idea: Score features by how often their values exceed 50% churn—simple but flawed.

Why It Failed:

- Doesn’t factor in how common each value is

- Ignores population impact

- Flat-scores binary fields

- Misses useful variance within a feature

FIG. E: Left: naive “value-over-threshold” filter. Right: properly weighted decision tree scores.

➡️ Takeaway: Early shortcuts can mislead. Standard deviation better captures features with real signal.

Recommendations

1. Use Credit Card Status as a Churn Flag

No-card customers exploring new products represent the highest churn risk.

2. Focus Retention on New Customers (≤3 Years Tenure)

Proactively survey or support this group—early dissatisfaction is high.

3. Reward Long-Tenure, Older Clients

Reinforce loyalty among your most stable customers (50+ years old, high tenure).

Tools Used: Excel, Lucidchart

Skills Demonstrated: Decision Tree Design, Ethical Data Handling, Churn Modeling, Feature Scoring